Dekpol SA - A quality company at a deep value price

A diversified group managed by a skilled owner-operator

Dekpol (DEK) mainly operates in the construction of commercial and industrial properties as well as residential development. Additionally, it engages in manufacturing within Prefab (partly to supply its own construction activities, partly for sales to external customers) and the production of steel machine components (primarily large buckets for the mining and construction industry). Dekpol's revenue is just under 1.6 billion PLN, and since 2015, it has shown an annual sales growth of 22%. Over time, the company has maintained an EBIT margin of 7% and has reported a positive bottom-line result every year since 2015.

The business is divided into three segments: General Contracting (72% of revenue), Development (13%), and Steel Structures (15%). Over 90% of the group's sales occur in the Polish market. In General Contracting, Dekpol offers turnkey solutions across all property sectors, with a recent focus on logistics properties. This segment has seen a CAGR of 18% and an average EBIT margin of 7%. In Development, the company develops apartments and aparthotels (premium segment) mainly in northern Poland, but recently also in Wroclaw and Warsaw. This segment has seen a CAGR of 29% and an average EBIT margin of 14%. In Steel Structures & Other, the company manufactures Prefab materials for the construction industry and construction machinery equipment, such as buckets, with clients including Hitachi, Volvo, Caterpillar, and Doosan. Russia's invasion of Ukraine significantly impacted this segment, causing the EBIT margin to drop from about 10% to 6% in 2022, and just under 2% in 2023. This segment has seen a CAGR of 40% (largely driven by acquisitions) and an average EBIT margin of 11%. Additionally, HQ has central net costs of about 10 million PLN per year (where some billing activity also takes place).

Dekpol was listed on the stock market in the winter of 2015 at 15 PLN per share. Those who have been with the company since the start have, including two dividends, had an annual return of 16%. The major shareholder is founder and CEO Mariusz Tuchlin with 77% of the shares. Tuchlin, a trained roofer, started Dekpol at the age of 19. Since 2017, the second-largest shareholder is Luxembourg-based Familiar S.A. Sicaf-Sif with 8%, which also owns stakes in the courier service Pointpack (8%) and the restaurant chain Mex Polska (6%). Familiar S.A. Sicaf-Sif is controlled by financier Grzegorz Szymanski. Therefore, the free float is limited to 15%.

Today, Dekpol is valued at P/TB 0.80 (compared to a historical average of 1.11) and P/E 5.0. Historically, ROE has averaged 19%, and TB/share has increased by 21% annually since 2015, despite two dividends in 2017 and 2018. Net gearing has decreased from 93% at IPO to 15% today (adjusted for "investment properties", the company has a marginal net cash position). Dekpol aims to have an ND/EBITDA of 2-3x, with covenants putting a stop at 4.5x ND/EBITDA – today, this multiple is 0.38x.

This indicates good conditions for offensive ventures (Dekpol has made three acquisitions since 2018) or future dividend possibilities. In a "status quo" scenario, the company will be debt-free by mid-2024. Alternatively, if we sketch a gearing corresponding to an ND/EBITDA of 2.5x, it implies that the company has "dry powder" of 338 million PLN. If they could perform an acquisition at 5x EBIT, it would result in EBIT increasing by 57% from 119 million PLN to 187 million PLN. Assuming an 8% interest rate, EBT would be 160 million PLN, and after 19% tax, 131 million PLN would remain in EAT, or EPS of 15.6 PLN – corresponding to a P/E ratio of 3.3.

Another, more theoretical option, would be a "dividend re-cap" where the company distributres say 200 million PLN of its current cash. This would give shareholders a dividend of 24 PLN, compared to the current price of 52 PLN. Equity ratio would decrease from 36% to - perhaps a slightly too weak - 26%. However, history deems this scenario highly unlikely – but it demonstrates the possibilities for quick value realization.

On the balance sheet, there are plenty of "relatively realizable" assets in the form of land, apartments, and a hotel. Under the PPE of 146 million PLN, there is land worth 19 million PLN, buildings worth 59 million PLN, and machinery and other fixed assets worth 68 million PLN. Under investment properties of 81 million PLN, there is land worth 13 million PLN and Hotel Almond in Gdansk (leased out until 2033) worth 68 million PLN (carried at a gross yield of just under 6%). Of the inventory of 430 million PLN, 191 million PLN consists of completed apartments and 185 million PLN of apartments under construction. Of the company's interest-bearing gross debt of 374 million PLN, 282 million PLN refers to issued bonds with various maturities and sizes of 30–60 million PLN. 174 million PLN of the interest-bearing debts are to be repaid/refinanced within the next 12 months, which the company can easily do with its current cash (326 million PLN).

(The wholly owned hotel, Hotel Almond in Gdansk. Source: Google Maps)

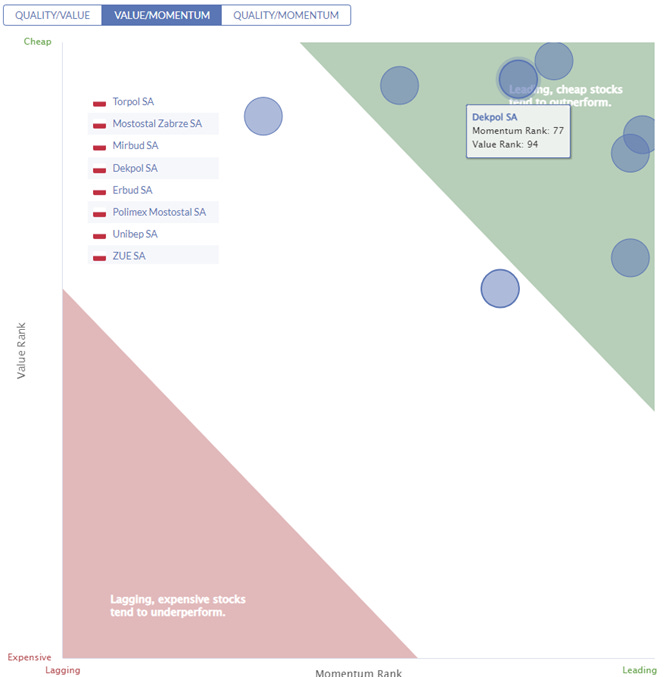

Comparing Dekpol with seven Polish peers (Erbud, Mirbud, Mostostal Zabrze, Polimex Mostostal, Torpol, Unibep, and Zue), Dekpol appears to be one of the better in class in terms of margins and growth (8% EBIT compared to 5% for the group and 22% 3y Sales-CAGR compared to 18% for the group) while being valued slightly lower than the average – 0.80x TB against the group's 1.13x and 3.9x EBITDA against the group's 7.5x. At the group's average multiples, Dekpol would be valued at 73-115 PLN/share, corresponding to an upside of 40%-120%. Looking at the peer group's "Stockopedia" positioning, it also seems to be a potentially good entry point for Dekpol and its sector.

One might wonder what Dekpol is actually doing on the stock market. For Tuchlin, it would have cost 100 million PLN to buy out the minority at the current market price. Say that a 50% premium was required, that is, 150 million PLN, to buy out the minority. This could easily be financed by the company, temporarily increasing its gearing (net gearing from 9% to 37%) and making a tender offer at 78 PLN per share for the minority's share. However, it's conceivable that the company benefits from being listed, with the quality stamp and public scrutiny that comes with it.

In the latest quarterly report, Dekpol describes that both the construction and housing markets are beginning to show signs of revival (not that the sector, according to the company's segment data, seems to have struggled too much in recent years). The order book within General Contracting amounted to 824 million PLN at the end of the period, compared to 323 million PLN during the same period the previous year. At the start of 2024, the Polish government launched the support program "Kredyt 2%" aimed at those under 45 years old who have never owned their own home. Within the program, these individuals can receive a ten-year loan of up to 500 thousand PLN at a fixed interest rate of 2%, which obviously might lead to positive "cascade effects" on the housing market. Dekpol has an ambitious goal to sell 650 apartments and turn over 400 million PLN within the development segment in 2024 (in 2021, 472 apartments were sold, and the segment turned over 278 million PLN).

The graph below shows the development of housing prices in Poland. It looks anything but "crisis". However, it's important to remember that inflation in 2021 was around 6%, in 2022 around 15%, and in 2023 around 10% - so in real terms, the situation looks quite different.

Historically, Dekpol has been valued in a broad range between P/TB 0.50 - 2.40. When the company closed the books for 2017, all stars were aligned. Revenue increased by 109% and net income by 133%. All segments performed well, and the company sold over 800 apartments. The Dekpol stock had the highest return of all stocks on the Warsaw Stock Exchange, up 260%, compared to WIG-Real Estate, which rose 20%, and WIG-Construction, which remained unchanged at 0%. Dekpol won a gazelle award, and Tuchlin was nominated for stock market CEO of the year. The valuation then peaked at P/TB 2.40.

Besides the short-lived "Covid crash", the company's historically lowest valuation (in terms of assets) was in the spring of 2022. The reason was, of course, Russia's invasion of Ukraine and the subsequent negative market trends in terms of disrupted supply chains, inflation, high interest rates, and general uncertainty. However, focusing on short-term contracts allowed the company, despite rising prices for materials and services, to maintain its margins. Thanks to its own production of concrete and steel prefabricates, it was also less affected than other industry players by the disrupted supply chains. Despite challenging market conditions, Dekpol showed a sales growth of 10% and a net income increase of 4% to 79 million PLN – the company's best yearly result at the time. However, “Mr. Market” was very negative, and the stock was valued at P/TB 0.40 in the spring of 2022.

After the invasion of Ukraine, parts of the Steel Structures & Other production were reoriented, and the process of acquiring licenses required to become a supplier to the defense segment, including NATO, was initiated – something that naturally opens up potentially lucrative opportunities in the future. At the same time, the solid development during 2022 showed that there is stability in the group's diversification. The fact that the construction as well as the housing markets are now showing signs of recovery, while the financial position has never been stronger (at least as a listed company), also suggests that Dekpol is well positioned to develop positively in the coming years. A turnaround has already been discerned during 2023 with an EPS growth (q/q) of 27% in 2Q23 and 44% in 3Q23. However, based on the preliminary figures communicated, EPS growth for 4Q23 appears to be at -27%.

Currently, the stock is historically relatively low valued, which leads us to assess that an investment has a sound risk/reward profile. And even though the sector "has started to move," it seems like Dekpol has so far lagged somewhat. In a scenario where the company maintains its current earnings level (which feels like a rather modest assumption), tangible equity will increase from 62 PLN/share to 86 PLN/share within two years, and the net cash will then be 16/share. We would be very surprised if Tuchlin allowed the cash to swell in that way; rather, aggressive business initiatives and/or dividends will likely be pushed through – two scenarios we like. It's also hard to see that the stock price under such a scenario would stay unchanged, as it would imply a P/TB multiple of 0.60 – a level at which Dekpol has only been valued at or below, during "deep unrest times" and only during 6% of the trading days since 2015.

(Disclaimer: at the time of publication, the writer owns shares in the mentioned company)