The Polish Deep Value Week – 2024/48

A few major project wins, weak reports and insider transactions

Companies mentioned

· Amica (AMC)

· Action (ACT)

· Compremum (CPR)

· Dekpol (DEK)

· Fasting (FSG)

· Izoblok (IZB)

· Izostal (IZS)

· Monnari Trade (MON)

· Mostostal Zabrze (MSZ)

· Pamapol (PMP)

· Remak Energomontaz (RMK)

· Rawlplug (RWL)

· Selena FM (SEL)

· Sanwil (SNW)

· Stalprofil (STF)

· Trans Polonia (TRN)

Benjamin Graham famously suggested that one way to measure the valuation of the overall market was to assess the number of net-nets available. The prevalence of net-nets serves as a barometer for market valuation. When many such opportunities exist, it indicates a cheap market overall, while their absence suggests that the market is expensive.

Below is this week’s net-net screen from Stockopedia. Note though that today’s net-nets are not the same as Graham’s net-nets. We view many of these as un-investable being loss-making biopharma’s etc. But even though we would not invest in a large part of today’s crop we think it could be interesting to follow this number over time, and what percentage of total listed stocks qualify as a “naked” net-net without any type of quality adjustments to make them investable. So, each week, we plan to hold “Graham’s Geiger counter” over our markets.

Amica – Declining revenues in q3 2024 but targets long-term profitability with new strategy

AMC │ New Report│ P/TB 0.56 │ Consumer Goods & Products│ URL

AMC reported mixed performance for 3Q24, with revenues declining 6% to 650 mpln compared to 691 mpln in the same period last year. The gross margin decreased slightly from 26.7% to 26.3% as well as the EBIT margin from 2.7% to 1.6%. Net income was –4.7 mpln (2.2 mpln). The bottom line was adversely impacted by higher financing costs and foreign exchange volatility.

The Group unveiled a new "Back to Profitability" strategy for 2024–2030+, focusing on enhancing product quality, operational efficiency, and geographic market penetration within Europe. The strategy includes clear financial targets, such as achieving an EBITDA margin of 5% by 2027 and 7% by 2030, alongside strengthened ESG initiatives, including investments in renewable energy via Amica Energia.

Outlook remains cautious, with the management emphasizing recovery plans amid ongoing market challenges. While cost-saving measures and a focus on core markets are expected to aid stabilization, achieving sustainable profitability will hinge on macroeconomic recovery and consumer sentiment improvement.

Action – Further buybacks

ACT │ Buybacks│ P/TB 0.70 │ Electronics Distribution│ URL

Between November 21 and November 27, 2024, the company repurchased a total of 15.6k shares for 276k, with an average unit price of 17.72 pln. The shares represent 0.09% of the company's share capital and voting rights. As of November 27, 2024, ACT holds a total of 1.2m treasury shares, constituting 7.2% of its share capital and voting rights.

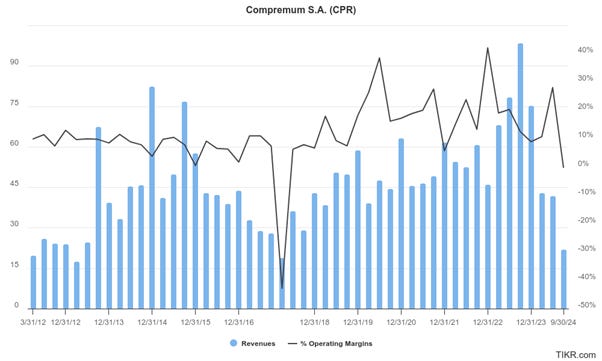

Compremum – Faces revenue decline and liquidity challenges amid construction delays in q3 2024

CPR │ New Report│ P/TB 0.30 │ Construction│ URL

CPR reported significant challenges in Q3 2024, with net revenue declining to 21.8 mpln, a steep drop compared to PLN 98.4 million in the same period last year. Gross profit from sales also decreased significantly, with a decline in gross margin from 13.1% to 7.7%. EBIT was 0.0 mpln (12.3 mpln) and net income was -1.8 mpln (7.4 mpln). The decline is attributed to reduced construction activity and delays in key contract executions. Sales as well as margins wise, the last quarter is one of the weakest the company has had in modern times.

The company is highlighting delayed invoicing cycles in construction projects as a key issue. The dependency on the GSM-R project was noted as a primary driver of liquidity strain, with completed work awaiting billing and payment. Management has emphasized that while no immediate threats to business continuity exist, ongoing delays could jeopardize cash flow stability in the coming months. However, looking at historical ratios, the liquidity as well as solidity situation seems to be quite manageable.

Looking ahead, CPR expects financial recovery through accelerated project deliveries and improved collections in 4Q24. Despite these hurdles, the management remains confident in its long-term growth strategy anchored in construction and renewable energy markets.

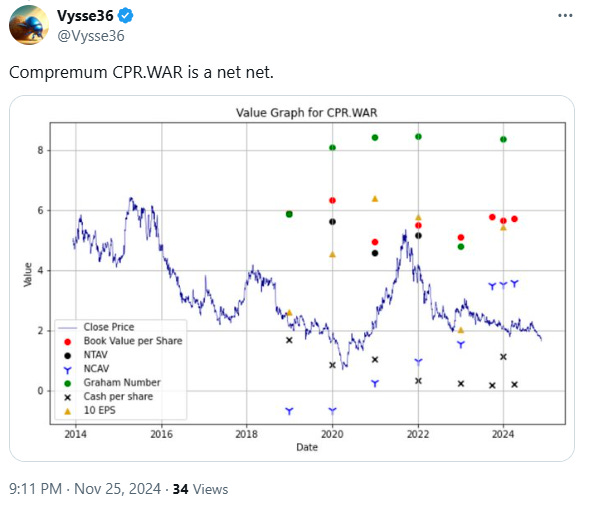

Finally, Vysse36 posted a valuation graph on the company.

Dekpol – New analysis, large distribution center project & bond re-financing

DEK │ Analysis│ P/TB 0.69 │ Construction│ URL / URL / URL / URL

Mattdeepvalue wrote a piece on the company - Investment Insight: Dekpol SA — Balancing Challenges and Opportunities.

DEK announced the signing of a letter of intent on November 22, 2024, through its subsidiary Dekpol Budownictwo Sp. z o.o., to undertake the general contracting of a distribution center in northern Poland. The investment is expected to be valued at approximately 31% of the Dekpol Group’s 2023 sales revenue (c. 486 mpln), with a targeted completion in 1Q26. While the letter of intent outlines key conditions, including remuneration and timelines, it is not legally binding. A final agreement is anticipated by December 2024.

The company also increased the maximum number of Series N bonds proposed for purchase to 102,569 units, with a total nominal value of 102.6 mpln. The bonds are unsecured and will mature within four years, with provisions for early redemption. DEK also announced the early full redemption of 70 mpln worth of Series P2023A and P2023B bonds, originally maturing in 2026. The early redemption of Series P2023A and P2023B bonds will be financed using proceeds from the issuance of Series N bonds.

Fasing – More business with Karbon 2

FSG │ Order│ P/TB 0.24 │ Mining Equipment│ URL

FSG has issued new orders to KARBON 2 Sp. z o.o. (the company’s majority shareholder with 60% of the shares) for rolled bars and wire rods valued at 1.6 mpln gross. This order continues the ongoing cooperation between the two companies, focused on the procurement of steel products essential for FSG’s operations. Since June 24, 2024, the cumulative value of orders placed by FASING with KARBON 2 has reached 14.3 mpln gross.

Izoblok – Achieves profit surge in q3 2024 amid revenue growth and strategic investments

IZB │ New Report│ P/TB 0.62 │ Plastic Moulding│ URL

IZB reported consolidated revenues of PLN 184.4 million for the first nine months of 2024, representing a 3.8% increase compared to the same period last year. This growth was driven by steady performance in the automotive segment, which accounted for most of the revenue, and robust gains in the packaging sector, which rose by 29%. Despite revenue growth, operational costs increased by 8.7%, reaching 192 mpln, primarily due to higher wages, energy prices, and external services costs.

EBITDA rose by 12.8% to 16 mpln, resulting in an EBITDA margin of 8.7%. Management noted that favorable operational efficiencies and strategic investments contributed to the improved profitability, despite sector-wide challenges such as rising input costs and production delays in the electric vehicle market. Net profit for the period surged to 17.4 mpln from 2.3 mpln in the previous year, supported by a one-time tax adjustment and cost optimization initiatives

The group maintained its focus on expanding its production capacity and securing key contracts. Notable strategic actions included investments in property divestments, which bolstered financial inflows. Management emphasized that ongoing initiatives aim to enhance operational independence and mitigate supply chain risks, particularly for essential materials.

Looking ahead, Izoblok expects stable performance supported by its diversified customer base and strategic growth investments. However, macroeconomic challenges, including high energy costs and market volatility, may temper profitability in the short term.

Izostal – New order

IZS │ Order│ P/TB 0.35 │ Steel Processing│ URL

IZS announced that a consortium it is part of has been selected for the construction of the Kalisz–Sieradz gas pipeline, a project organized by Polska Spółka Gazownictwa sp. z o.o. The consortium, led by STF Infrastruktura Sp. z o.o., includes Gascontrol Polska Sp. z o.o. and Izostal S.A. The selected offer has a gross value of 218 mpln (177 mpln). The project involves the construction of a DN 500 MOP 6.3 MPa gas pipeline spanning approximately 62 km and additional infrastructure within 25 months of the Ordering Party's co-financing agreement.

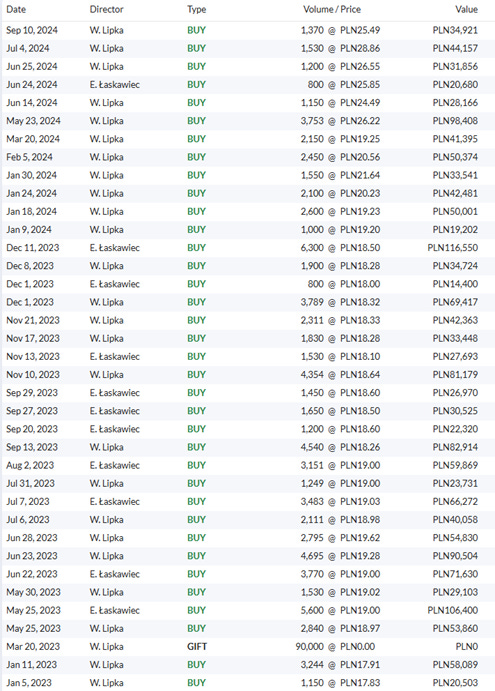

Kompap – Insider transactions

KMP │ Insider Transactions│ P/TB 1.37 │ Paper │ URL / URL

Piotr Ciosk, a member of the Supervisory Board, has reported on the sale of company shares. The transaction involved 3,268 shares at a price of 22 pln per share, totaling 71.9k pln. Waldemar Lipka, the President of the Management Board, has reported several transactions involving the company’s shares. On November 22, 2024, Lipka acquired a total of 3,600 shares at an average price of 21.99 pln per share. On November 26, 2024, he purchased an additional 200 shares at PLN 22 each. On the same day, November 26, 2024, Waldemar Lipka also sold 200 shares at PLN 22 per share.

KMP has a strong history of insider purchases and especially Lipka (32.3% shareholding) and Laskawiec (23.6%) have slowly been increasing their positions in the company.

Monnari Trade –3Q24

MON │ New Report│ P/TB 0.48 │ Apparel│ URL

Monnari Trade S.A. reported consolidated revenues of 219 mpln for the first nine months of 2024, reflecting a modest increase of 1.9% compared to 215 mpln during the same period in 2023. Retail sales in physical stores contributed to the revenue, while online sales grew to 36.7 mpln, a 5.3% year-on-year increase. For the third quarter, sales decreased 2.7% to 70.7 mpln (72.7 mpln). Gross profit increased to 41.6 mpln (41.2 mpln), corresponding to a gross margin of 58.8% (56.7%). However, due to increasing SGA costs, the EBIT margin turned negative at -0.5% (2.7%).

Looking ahead, Monnari aims to strengthen its market position through ongoing investments in e-commerce and physical store networks. Management has highlighted a cautious approach to cost management and inventory optimization to navigate persistent inflationary challenges and maintain profitability in a competitive retail environment.

Mostostal Zabrze – Entered into a new project

MSZ │ New Project│ P/TB 1.16 │ Construction│ URL

MSZ announced that its subsidiary, Mostostal Zabrze Realizacje Przemysłowe S.A. (MZRP), has entered into a significant agreement with IONWAY Poland Sp. z o.o. The contract, signed on November 26, 2024, pertains to mechanical works, equipment assembly, and technological pipeline installation as part of the Blue East W1 Project at IONWAY’s plant in Radzikowice near Nysa. The agreement's value corresponds to approximately 10% of Mostostal Zabrze Capital Group’s 2023 sales revenues (c. 135 mpln).

The project has a completion deadline set for the end of March 2026, with contractual terms that cap MZRP’s liability for penalties and damages at 100% of the net remuneration, excluding intentional damages. Standard clauses include the Ordering Party's right to seek additional compensation and withdraw from the agreement in specific cases. In scenarios where withdrawal is not attributed to MZRP, the Ordering Party must compensate for completed works.

Pamapol –Faces revenue decline and losses in 2024, banking on strategic investments for recovery

PMP │ New Report │ P/TB 0.59 │ Food & Nutrition│ URL

PMP reported revenues of 229 mpln (230) for the third quarter. The gross profit amounted to 42.1 mpln (38.2 mpln), corresponding to a gross margin of 18.3% (16.6%). EBIT was -1.0 mpln (4.5mpln) and net income decreased to -5.3 mpln (0.4 mpln),

Key factors impacting performance included inflationary pressures, elevated interest rates, and unfavorable currency fluctuations, which negatively affected export margins and increased production costs. Prolonged negotiations with key retail customers led to delays in price adjustments, further impacting profitability. Additionally, one-off events such as intensified competition required inventory clearances at lower prices, incurring additional losses.

Strategic initiatives are underway to address challenges. Investments in the Mitmar facility aim to enhance production capacity with a focus on new product categories, expected to commence fully in Q4 2024. The Group has also intensified cooperation with financial institutions to restructure debt covenants and secure additional funding to support growth plans and stabilize liquidity. Looking ahead, PMP remains cautious about short-term macroeconomic uncertainties but anticipates improved results as strategic investments begin yielding returns.

Remak Energomontaz –Secures 1.8 mpln contract increase for ArcelorMittal renovation project

RMK │ New Order│ P/TB 0.48 │ Industrial Services│ URL

RMK has announced the conclusion of Annex No. 2 to an agreement with ArcelorMittal Poland SA. This agreement, initially reported in 2022, involves a consortium led by Remak-Energomontaż and Zarmen sp. z o.o., for renovation works on the K3 - ECII Zdzieszowice boiler at the Ordering Party's branch in Zdzieszowice. The newly signed annex increases the total remuneration for the project to 43 mpln net, representing an additional 1.8 mpln net.

Rawlplug – Reports resilient performance amid declining revenues, focuses on strategic growth opportunities

RWL │ New Report│ P/TB 0.96 │ Fasteners│ URL

RWL reported revenue of 290 mpln (295 mpln) for 3Q24. EBIT was 33.0 mpln (24.7 mpln), corresponding to an EBIT margin of 11.4% (8.4%). Net profit for the period reached 15.3 mpln (9.6 mpln). YTD Domestic sales saw significant growth of 9.9%, driven by robust demand in Poland. However, export sales fell by 12.7% to due to weaker performance in European markets. Export sales accounted for 66.2% of total revenues. The product segment's share in total revenue increased to 63.7%, up from 61.9%, reflecting the company’s focus on higher-margin offerings.

Looking ahead, management highlighted challenges from fluctuating demand in the European construction market but noted growth opportunities in Asia, Africa, and Australia. Key strategic priorities include maintaining high product availability, cost optimization, and expanding market presence through e-commerce and new product launches. The implementation of a new ERP system in 2025 is expected to enhance operational efficiency. Despite these efforts, the company remains cautious due to rising costs and competitive pricing pressures globally.

Selena FM – Reports mixed q3 2024 results with strong 9-month growth and margin improvement

SEL │ New Report│ P/TB 0.98 │ Construction│ URL

Selena FM Group's consolidated financial results for Q3 2024 indicate a mixed performance in a challenging market environment. For the first nine months of 2024, the Group achieved total revenue of 1,358 mpln, marking a marginal year-on-year increase of 0.1%. Gross profit rose by 6% to 464 mpln, with the gross margin improving to 34.2%, reflecting a stronger focus on higher-margin product lines. Operating profit (EBIT) reached PLN 123.1 million, a notable increase of 23.4% compared to the prior year, driven by efficiency measures and improved product profitability.

For the last quarter, sales decreased by 1.8% to 483 mpln (492 mpln) and EBIT decreased to 51.6 mpln (69.4 mpln, corresponding to an EBIT margin of 10.7% (14.1%). The net profit for the quarter fell sharply by 54.6% to PLN 24.95 million, primarily due to increased financial costs and unfavorable currency fluctuations.

Looking ahead, Selena FM Group remains cautiously optimistic, focusing on the growth of innovative and high-margin product lines despite ongoing macroeconomic challenges, such as currency fluctuations and a global slowdown in the construction sector. Cost optimization and operational efficiency remain key priorities to navigate the uncertainties and maintain profitability in the coming quarters.

Sanwil – 3Q24

SNW │ New Report│ P/TB 0.38 │ Coated Fabrics│ URL

SNW reported a decrease in sales of 18.7% to 6.2 mpln (7.6 mpln) for 3Q24. EBIT was -0.4 mpln (0.7mpln), corresponding to an EBIT margin of -6.5% (9.2%). YTD, sales were down to 21.1 mpln (24.9 mpln). The coated fabrics segment accounted for 12.9 mpln in upholstery sales, which saw a notable decrease from 14.6 mpln in 2023. Domestic revenues dropped by 13.5% year-over-year, while export markets grew by 32%, driven by gradual recovery in demand from Ukraine and intensified activities in Western Europe. The domestic market remains a primary focus, although heightened competition has eroded profitability.

The company is optimistic about export market growth but remains cautious about domestic market recovery due to ongoing competition and macroeconomic pressures. Strategic initiatives include enhancing technological capabilities, introducing new product lines, and pursuing partnerships to improve market positioning. The company is also reviewing strategic options, including divesting non-core assets and expanding its research and development efforts.

SNW highlighted risks such as currency fluctuations, raw material price volatility, and geopolitical instability, particularly regarding the Ukrainian conflict. To mitigate these challenges, the company is focusing on operational efficiency, expanding its market reach, and maintaining long-term supplier agreements for stability. Additionally, investments in innovation aim to align product offerings with evolving market demands.

Stalprofil – 3Q24

STF │ New Report│ P/TB 0.31 │ Steel Processing│ URL

The company’s Q3 2024 financial report highlights a modest decline in revenues and net profitability. Net sales amounted to 323, down 12.7% compared to 370 mpln for the same period last year. The gross profit margin increased to 9.1% (6.8%). Operating profit for 3Q24 was 6.8 mpln, up from 6.0 mpln last year. Net profit also increased to 3.7 mpln (2.1 mpln).

Outlook remains cautious, with the management acknowledging the prolonged downturn in the steel market. Demand forecasts for 2024 have been revised downward to a 1.5% contraction, signaling continued challenges in restoring pricing power and volume growth. Investment in logistics and operational resilience, however, positions the company for improved performance in eventual market recovery phases.

Trans Polonia – 3Q24

TRN │ New Report│ P/TB 0.39 │ Transportation│ URL

TRN reported a 10.7% year-over-year increase in net sales revenue for 3Q24, reaching 57.6 mpln (52.1 mpln). The growth was primarily driven by strong performance in the transportation of liquid chemicals and food products. EBIT also increased to 3.1 mpln (2.0 mpln), corresponding to an EBIT margin of 5.5% (3.8%).

Looking ahead, the group projects continued revenue growth, particularly in chemical logistics within Western Europe. However, management highlighted risks such as fluctuating fuel prices and increasing labor costs, which may put pressure on margins.

The writer may own shares of the companies mentioned. This communication is for informational purposes only.