The Polish Deep Value Week – 2025/08

New Report, Buybacks and New Contracts

Companies mentioned

· Dębica (DBC) - Recovers Production Capacity, Reports PLN 2.56 Billion Revenue for 2024

· Monnari Trade (MON) – Further Buybacks

· Remak-Energomontaż (RMK) - Signs PLN 23 Million Agreement with ORLEN Termika

· Stalprofil (STF) – New Contract & Estimated 4Q Figures

· Stalprodukt S.A. (STP) - Reports Significant Profit Growth in Q4 2024

· Werth-Holz (WHH) - Reports Revenue Growth but Sustained Losses in Q1 2024/2025

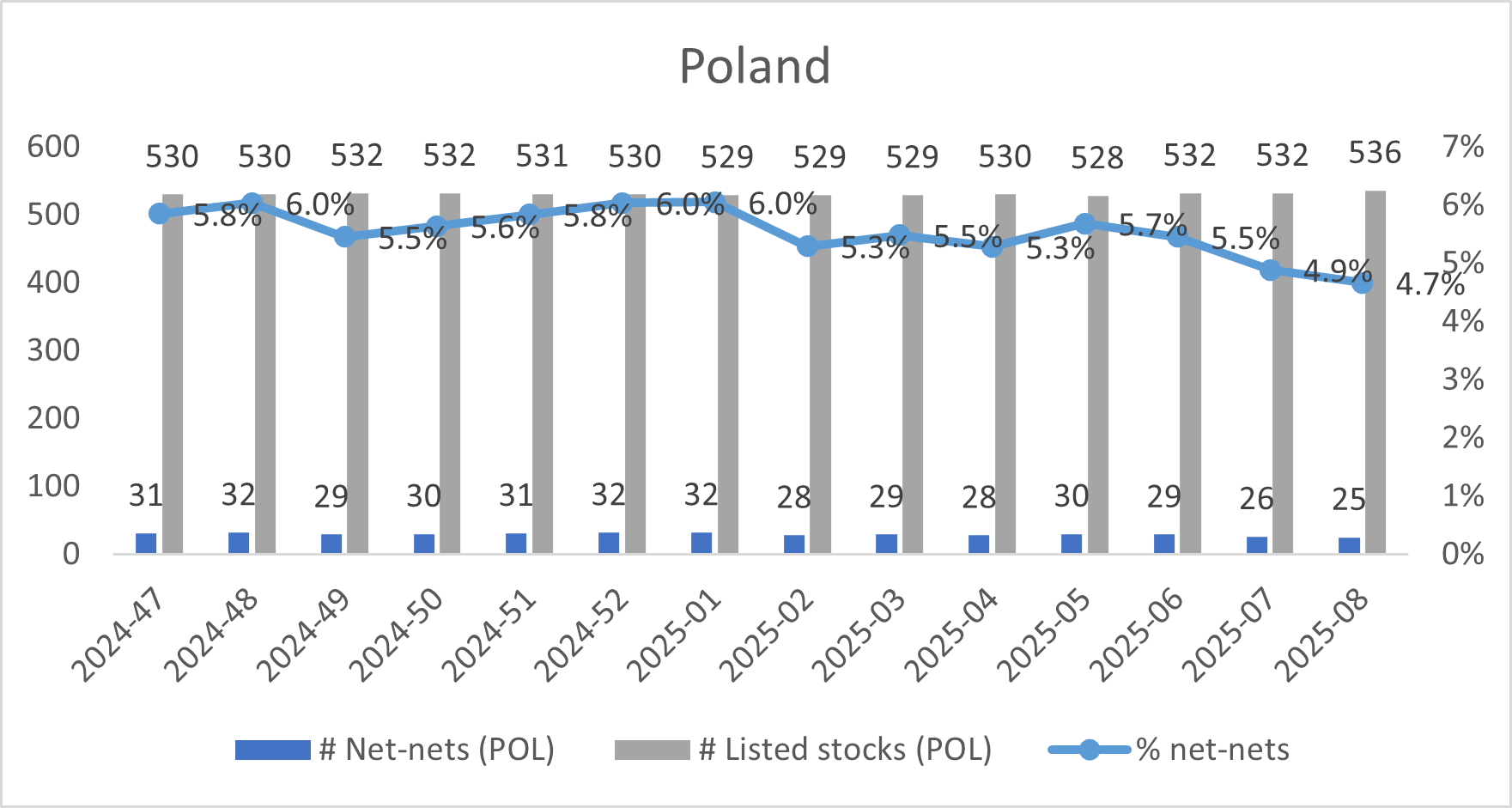

“Graham’s Geiger counter”

Benjamin Graham suggested that one way to measure the valuation of the overall market was to assess the number of net-nets available. When many such opportunities exist, it indicates a cheap market overall, while their absence suggests that the market is expensive. Today’s net-nets, however, are not the same as Graham’s net-nets. Many are un-investable being Chinese RTO’s, loss-making biopharma’s etc. But we do think it is interesting to follow this number over time, and what percentage of total listed stocks qualify as a “naked” net-net without any type of quality adjustments to make them investable. Below is a net-net screen from Stockopedia.

Dębica (DBC) - Recovers Production Capacity, Reports PLN 2.56 Billion Revenue for 2024

P/TB 0.84 │ URL

Tire Company Dębica S.A. has announced its preliminary financial results for 2024, with net revenue from sales of products, goods, and materials reaching PLN 2,556.9 million and a net profit of PLN 77.8 million. The company's financial performance was influenced by several key factors, including limited production capacity and lower sales prices in transactions with related entities. These pricing adjustments were a result of decreased raw material costs in late 2023, which impacted pricing calculations in the first quarter of 2024. Additionally, other operating income was positively affected by an advance compensation payment of PLN 151 million related to the fire incident in August 2023. However, ongoing costs associated with the fire, including unused production capacity and rebuilding efforts, amounted to PLN 108 million for the year. The company successfully restored its full pre-fire production capacity in the fourth quarter of 2024.

Dębica’s management emphasized that the presented results are estimates and may differ from the final audited figures, which will be published on April 25, 2025. The current values were obtained during the financial statement preparation process and are subject to audit, which may result in adjustments. Despite the challenges faced throughout the year, the company’s recovery and return to full production capacity are expected to support future growth and operational stability.

Monnari Trade (MON) – Further Buybacks

P/TB 0.45│ URL

MONNARI TRADE S.A. has reported the acquisition of 18,704 shares of its own stock on the Stock Exchange between February 17 and February 21, 2025. The transactions were conducted through the Brokerage House of mBank S.A. as part of the buyback program authorized by Resolution No. 14 of the Annual General Meeting on June 16, 2023. The shares, each with a nominal value of PLN 0.10, were purchased at an average price of PLN 5.12 per share. Following these acquisitions, the Issuer holds a total of 5,335,468 shares, representing 17.46% of the company’s share capital and entitling to 15.18% of votes at the General Meeting.

Remak-Energomontaż (RMK) - Signs PLN 23 Million Agreement with ORLEN Termika

P/TB 0.56 │ URL

Remak-Energomontaż S.A. (“Issuer,” “Company,” “Contractor”) announced that on February 18, 2025, it signed an agreement (“Agreement”) with ORLEN Termika S.A., headquartered in Warsaw (“Ordering Party”). The Agreement entails the mechanical overhaul of the Tz-7 turbine set at the Siekierki CHP Plant, including the supply of necessary materials, spare parts, equipment, devices, structural elements, and installations. The scope also covers preparatory documentation, technical implementation, and as-built documentation.

The contractual net remuneration is PLN 22,995,000.00, calculated as-built based on lump sum unit prices specified in the Agreement. Work is set to commence immediately following the agreement's signing, with an expected completion date of December 19, 2025. Contractual penalties imposed by the Ordering Party are capped at 30% of the net remuneration, while the Contractor's total liability for all penalties and damages, including lost profits, is limited to 100% of the net remuneration. However, this limitation does not apply to penalties related to damage, destruction, or loss of equipment.

Stalprofil (STF) – New Contract & Estimated 4Q Figures

P/TB 0.31 │ URL

STALPROFIL S.A. announced that on February 14, 2025, it signed an agreement with Gas Transmission Operator Gaz-System S.A. for the construction of a DN500 MOP 5.5 MPa high-pressure gas pipeline on the Oświęcim-Szopienice-Tworzeń route. The construction works will cover a 3 km section from Łąkowa Street in Imielin to ZZU KZ0505 in Mysłowice. The total value of the agreement is PLN 27.3 million gross, with project completion expected within 24 months from the contract signing date.

STALPROFIL also released its preliminary financial results for Q4 and full-year 2024. In Q4, the company reported a 66% year-on-year increase in sales revenue but an 85% drop in net profit. For the full year, sales revenue reached PLN 1,044 million (+13% YoY), while net profit stood at PLN 9.4 million (-27% YoY). The steel distribution market faced declining steel prices and narrow margins, with the average price of HEB 200 profiles down 4.5% YoY in Q4 and 14.3% YoY for the full year. However, STALPROFIL’s gas infrastructure segment performed well, benefiting from renewed investments, including projects related to the FSRU gas terminal. This segment significantly supported the company's financial performance, helping it achieve a satisfactory net profit despite market challenges. The final audited results will be published on April 25, 2025.

Stalprodukt S.A. (STP) - Reports Significant Profit Growth in Q4 2024

P/TB 0.37 │ URL

Stalprodukt S.A. has released preliminary financial results for Q4 2024, revealing significant deviations compared to the average values from the same quarter over the last two years. The consolidated operating profit reached PLN 65.5 million, marking a substantial increase from the two-year average of PLN 13.8 million. The consolidated net profit rose to PLN 57.2 million, compared to the two-year average of PLN 11.2 million. Meanwhile, the revenues of the Sheet Metal Segment stood at PLN 248.1 million, reflecting a decrease from the two-year average of PLN 366.5 million.

The improvement in profitability was primarily driven by stronger performance in the Sheet Metal and Zinc Segments compared to Q4 2023. Additionally, sectoral compensations received by Stalprodukt S.A. and its subsidiary, Huta Cynku “Miasteczko Śląskie” S.A., contributed positively to the financial results. These compensations were previously disclosed in Current Report No. 14 dated October 31, 2024. The disclosed figures are preliminary and were prepared as part of the company’s ongoing consolidation procedures. The final consolidated quarterly report for Q4 2024 will be published on February 28, 2025.

Werth-Holz (WHH) - Reports Revenue Growth but Sustained Losses in Q1 2024/2025

P/TB 0.45 │ URL

Werth-Holz SA capital group has published its consolidated financial results for the first quarter of the 2024/2025 fiscal year, covering the period from October to December 2024. The group reported an increase in revenue to PLN 6.167 million, up from PLN 4.256 million in the same period of the previous year. This growth was driven by the parent company’s performance in the wooden garden products segment, which saw an increase of PLN 2.42 million. However, subsidiary Enoviahaus Sp. z o.o., specializing in timber-frame construction, experienced a revenue decline of PLN 0.51 million due to the postponement of some contracts to later quarters.

Despite higher sales, Werth-Holz recorded an operating loss of PLN 716.8 thousand, compared to a loss of PLN 246.5 thousand a year earlier. The net loss widened to PLN 955.9 thousand from PLN 426.2 thousand in the previous year. The company attributed these losses to the high costs of financing inventory, as many retail clients postponed their initial orders to align with the spring sales season. Looking ahead, Werth-Holz aims to expand its dropshipping partnerships with DIY chains and increase direct online sales outside Poland. However, the profitability of its garden products segment will continue to be impacted by factors such as rising labor costs, high energy and wood prices, and the strength of the złoty. In the timber-frame construction segment, the company anticipates ongoing challenges due to the downturn in the German construction market, where building permits dropped by 21% in the first half of 2024. High land prices, rising construction costs, and high interest rates are expected to continue affecting demand in 2025.

The writer may own shares of the companies mentioned. This communication is for informational purposes only.